[ad_1]

FrozenShutter

After the market closes on November eighth, the administration workforce at The Walt Disney Firm (NYSE:DIS) is anticipated to report monetary outcomes masking the ultimate quarter of the corporate’s 2022 fiscal yr. Whereas the market has been challenged this yr amidst fears related to mounting inflation and rising rates of interest, some corporations have been hit tougher than others. This explicit agency is a good instance of that, as evidenced by the truth that shares are down 35.7% yr up to now as of this writing. For sure, traders may use a win. From a purely basic perspective, The Walt Disney Firm has been delivering properly this yr. However in fact, that image may change from quarter to quarter. And main as much as the fourth quarter earnings launch, there are just a few gadgets that traders ought to pay explicit consideration to. Though it is potential the market may ignore sturdy efficiency identical to it has for many of this yr, finally the tide ought to change for the higher as long as power persists.

Maintain a watch out on streaming

Though The Walt Disney Firm is a real leisure conglomerate, with many giant enterprises beneath its umbrella, there isn’t any denying that an important a part of the agency proper now could be the streaming portion of the enterprise. This has been a supply of great progress for the corporate and it has the potential, finally, to generate sturdy recurring money flows for the enterprise. Due to this, traders can be sensible to concentrate to what sort of subscriber numbers and different information the corporate studies when earnings do come out.

Writer – SEC EDGAR Knowledge

Usually, the streaming house has additionally confronted some challenges this yr. As an illustration, streaming large Netflix (NFLX) reported subscriber declines in two completely different quarters this yr earlier than posting sturdy outcomes lately. With shoppers stretched by excessive prices and a smorgasbord of streaming providers, there was substantial doubt in regards to the potential of sure streaming suppliers to satisfy their long-term goals. Even The Walt Disney Firm has been impacted by this. When the corporate reported outcomes for the third quarter this yr, it mentioned that it was lowering its 2024 goal for the worldwide Disney+ subscriber rely to between 215 million and 245 million in comparison with the prior anticipated vary of between 230 million and 260 million.

Whereas this is perhaps disappointing, it’s value noting that it nonetheless would indicate vital progress over the following a number of quarters. On the finish of the third quarter this yr, Disney+ had 152.1 million subscribers. That was up 14.4 million, or 10.5%, in comparison with the 137.7 million that have been on its roster only one quarter earlier. It could be extremely attention-grabbing to see if the platform can obtain continued sturdy progress on condition that financial situations appear to be worse now than they have been three months in the past. Nevertheless it’s not simply Disney+ that traders must be taking note of. ESPN+ is one other one of many firm’s streaming providers. Within the newest quarter, the service had 22.8 million subscribers. That was 500,000 larger than what was reported within the second quarter of this yr. In the meantime, Hulu reported 46.2 million, a rise of 600,000 in comparison with the 45.6 million reported just one quarter earlier.

Writer – SEC EDGAR Knowledge

The variety of subscribers reported by the corporate is unbelievably essential. Nevertheless it’s not the one factor that traders must be maintaining a watch out for. They need to even be taking note of the quantity of income per consumer per 30 days generated by every service. Within the third quarter of this yr, for example, Disney+ garnered $4.35 per consumer per 30 days. That was flat sequentially and up from the $4.16 per consumer per 30 days reported one yr earlier. ESPN+ noticed pricing of $4.55 per consumer per 30 days. That is a lower from the $4.73 per 30 days reported only one quarter earlier. And Hulu noticed pricing fall from $19.58 per consumer per 30 days within the second quarter of this yr to $19.41 per consumer per 30 days within the third quarter. What shall be actually attention-grabbing is how all this stacks up when you think about that, as a part of its third quarter earnings release, The Walt Disney Firm introduced plans to extend prices on its choices. As an illustration, the ad-free model of Disney+ rose from $7.99 per 30 days to $10.99 per 30 days within the US. The corporate additionally launched an ad-supported model of $7.99 per 30 days. There have been vital different modifications introduced as nicely, with plans to introduce mentioned modifications over time. Add on prime of this continued worldwide growth into markets that typically have lower cost factors than what extra developed markets have, and it stays to be seen what sort of pricing and subscriber progress the corporate’s numerous platforms can obtain.

Restoration is essential

As I discussed already, I view the streaming portion of the enterprise to be essentially the most important right now. Having mentioned that, there are parts of the enterprise that, as of the third quarter of this yr, have been nonetheless recovering from the COVID-19 pandemic. The trajectory of restoration for these numerous parts of the corporate will go a protracted technique to figuring out if the corporate is again to full well being and, if not, how lengthy getting again to full well being may take.

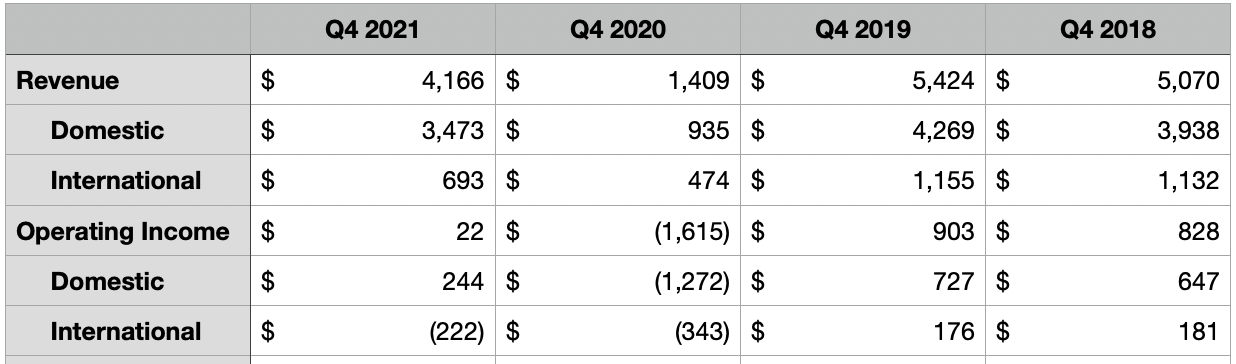

When speaking in regards to the areas most affected, the very first thing that involves thoughts is the Parks & Experiences portion of the corporate. Within the third quarter of this yr, the corporate’s parks noticed visitors will increase 69% relative to the identical time a yr earlier. Domestically, that quantity was far larger at 93% whereas the worldwide operations of the agency totaled solely 17%. The occupancy charge of home accommodations on the parks was at 90% in comparison with 50% seeing just one yr earlier, whereas in worldwide markets it stood at 61% in comparison with 20% a yr earlier than. It is protected to say that some significant disparity between home and worldwide operations will nonetheless exist from an admittance perspective. I say this largely due to the latest improvement of Shanghai Disneyland being compelled into lockdown due to COVID.

In what is perhaps a superb signal for shareholders, administration did announce value hikes earlier this yr for its home parks, together with on October eleventh. Whereas the decrease finish of the value vary of $104 for Disneyland has remained unchanged since 2019, there have develop into fewer and fewer days the place this value has been made obtainable. By comparability, a single-day ticket in California that permits entry to 1 park throughout a busy season like Christmas has jumped from $164 to $179. If you wish to add the power to hop between Disneyland and Disney California Journey, that prices an additional $65 in comparison with the additional $60 it used to value. These are simply among the examples of value modifications that the information has identified. Whereas actually painful to these wanting to go to, I say this might be a constructive as a result of it might be in response to sturdy attendance figures.

Writer – SEC EDGAR Knowledge

It is going to be very attention-grabbing to see how the monetary aspect of the image seems. To place this in perspective, take into account that within the third quarter of this yr the corporate’s Parks & Experiences operations noticed income of $6.21 billion. That was up from the $3.18 billion reported one yr earlier and from the $329 million reported within the third quarter of 2020. It was even larger than the pre-pandemic 2019 fiscal yr when the corporate reported gross sales of $5.55 billion. it is possible {that a} comparable development shall be seen this time round. Needless to say within the final quarter of the corporate’s 2021 fiscal yr, these operations reported income of $4.17 billion. That compares to the $1.41 billion reported the identical time of the 2020 fiscal yr. And with these income figures will even come essential working earnings figures as nicely. An analogous development will be seen on that entrance, with vital differentiation between home and worldwide operations.

Writer – SEC EDGAR Knowledge

*$ in Tens of millions

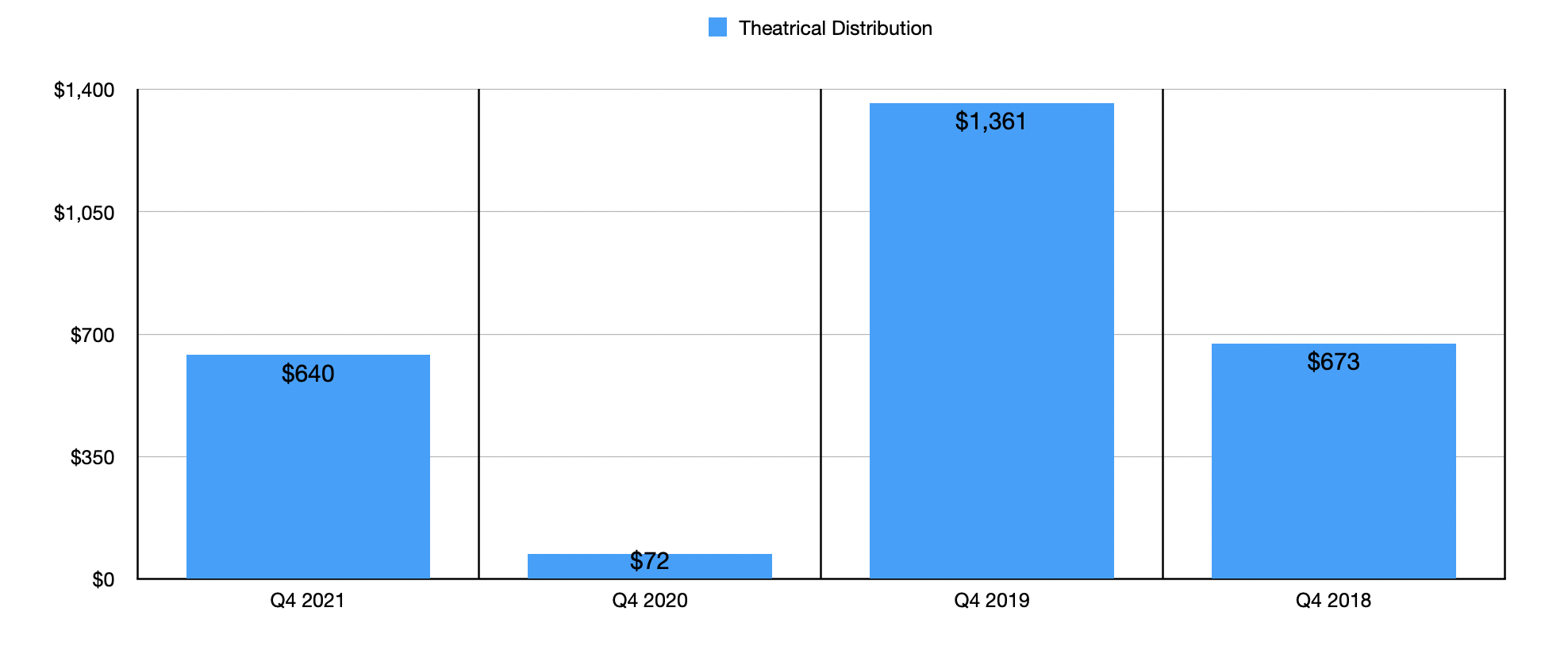

After all, the Parks & Experiences portion of the corporate isn’t the one portion that has been considerably impacted by COVID-19. We must also be taking note of the Theatrical Distribution aspect of the corporate. Within the third quarter of this yr, income of $620 million got here in larger than the $140 million reported one yr earlier and the $51 million reported within the third quarter of 2020. As for the fourth quarter, income within the 2021 fiscal yr got here in at $640 million. That is up considerably from the $72 million reported within the ultimate quarter of 2020. On the identical time, nevertheless, it was nonetheless down from the $1.36 billion skilled within the ultimate quarter of 2019.

A continued give attention to key metrics

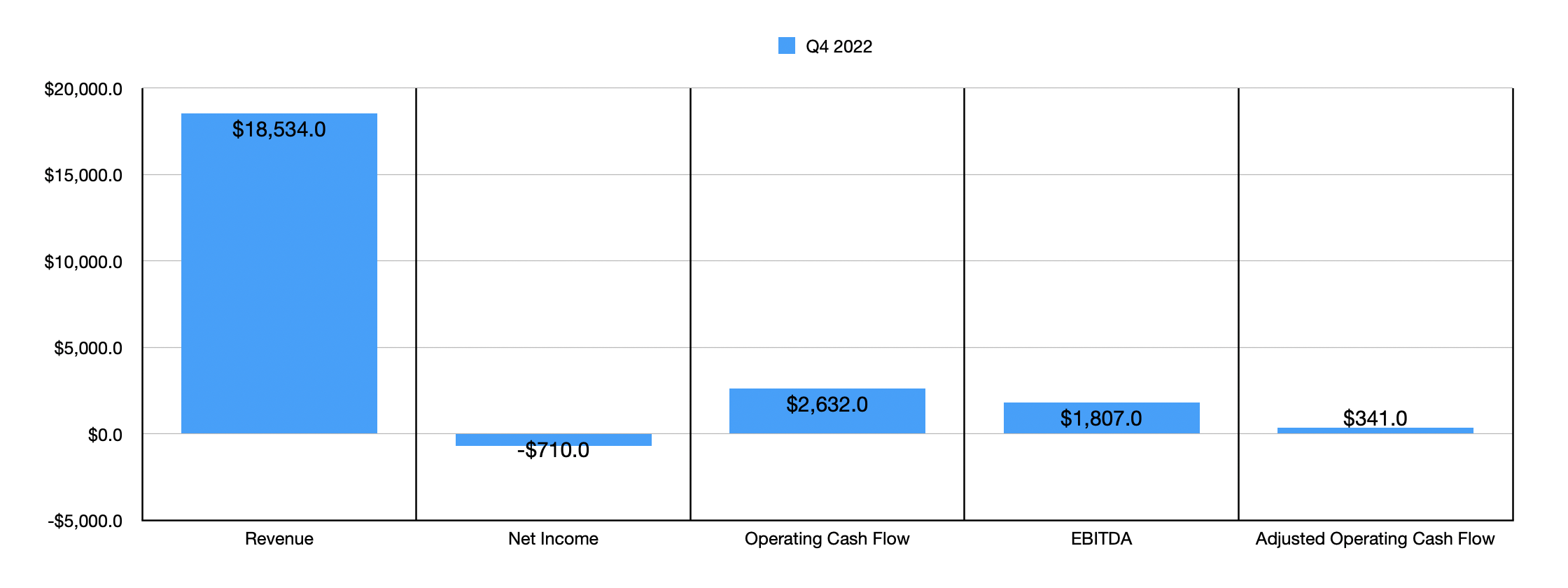

The final huge factor that I imagine traders ought to pay cautious consideration to can be how nicely the corporate performs basically. What I imply by this particularly is from a money circulation perspective. Final yr, the fourth quarter for the corporate was notably interesting, with the agency producing money circulation of $2.61 billion. That was up from the $1.47 billion reported just one quarter earlier. What’s actually attention-grabbing is that within the third quarter this yr, the corporate reported working money circulation of $1.92 billion. This implies that we is perhaps in for a slightly constructive ultimate quarter of this yr, particularly if streaming performs nicely and the elements of the enterprise that have been hit hardest by the COVID-19 pandemic additionally present enchancment.

Writer – SEC EDGAR Knowledge

In addition to simply serving as a measure of worth for the corporate, the opposite purpose why I like to have a look at working money circulation is as a result of I am thinking about whether or not the corporate will use it to scale back leverage or not. In any case, in 4 of the previous 5 quarters, administration has completed nicely to scale back internet leverage. On the finish of the third quarter, whole leverage was $38.64 billion. And within the ultimate quarter of 2021, it got here in barely decrease at $38.45 billion. Though I would not name The Walt Disney Firm over-leveraged, it’s all the time good to see debt lower because it finally lowers the danger for traders.

Traders must also take note of headline information gadgets like income and earnings. At current, analysts anticipate income from the corporate of $21.44 billion. That might signify a major enhance over the $18.53 billion the corporate generated within the fourth quarter of its 2021 fiscal yr. Earnings per share, in the meantime, must be $0.34 with adjusted earnings of $0.56. By comparability, the agency generated a loss per share in final yr’s ultimate quarter of $0.39. In absolute greenback phrases, the agency’s internet loss in final yr’s fourth quarter totaled $710 million. If analysts are proper this time round, the agency’s internet revenue for the quarter ought to whole $619.8 million, with adjusted income coming in larger at $1.02 billion.

Writer – SEC EDGAR Knowledge

Takeaway

I do know the instances are troublesome out there proper now. Actually, traders are apprehensive about what the longer term holds. Having mentioned that, I stay very assured in The Walt Disney Firm and I imagine that the trajectory for the corporate will stay constructive but once more. After all, it is unlikely that the quarter as an entire shall be good. However as long as the corporate can knock out some crucial classes, notably these associated to what I mentioned on this article, I imagine that it’s going to nonetheless signify a ‘sturdy purchase’.

[ad_2]

Source link